- The paper demonstrates a novel approach using deep neural networks to forecast future company fundamentals, achieving a 17.1% annual return compared to 14.4% from traditional models.

- It employs multi-task learning with MLPs and RNNs to predict multiple financial metrics, which reduces forecast errors and mitigates overfitting.

- The simulation strategy integrates predicted EBIT into factor models, yielding improved Sharpe ratios and robust performance across varied market conditions.

Improving Factor-Based Quantitative Investing by Forecasting Company Fundamentals

Introduction

The paper discusses an advanced strategy for quantitative investing, leveraging deep neural networks to predict future company fundamentals. By forecasting these fundamentals, the approach seeks to improve on traditional factor-based investment strategies, which typically rely on current financial data. The authors motivate this approach through simulations with a hypothetical clairvoyant model, highlighting the potential for significant gains when future data is utilized.

Methodology

Data Collection and Preprocessing

The study examines a dataset comprising 11,815 publicly traded stocks on the NYSE, NASDAQ, and AMEX exchanges, excluding non-US-based, financial sector companies, and those with market capitalizations below $100 million. Features were assembled from Compustat databases, with financial data discretized to monthly time steps and supplemented by momentum indicators over various time spans. All fundamental features were normalized relative to the company's size, using the market capitalization to ensure consistency across scales.

Model Architecture

The paper explores Multi-Layer Perceptrons (MLPs) and Recurrent Neural Networks (RNNs), specifically GRU and LSTM cells, to predict future fundamentals. Both models are evaluated for various configurations of hidden units and layers, optimizing architecture and learning parameters over an extensive hyperparameter space. The choice of using multitask learning, by predicting multiple future fundamentals, provides a robust signal potentially mitigating overfitting, especially compared to direct price prediction models.

Simulation Strategy

Investment simulations are conducted using a lookahead factor model (LFM), predicted through the neural networks for future fundamentals. Portfolios are created and managed using the traditional EBIT/EV factor, adjusted to include predictions from the LFM instead of current data. The authors rigorously backtest these strategies against standard factor-based models and a naive benchmark, simulating realistic transaction costs and market conditions.

Figure 1: Out-of-sample performance for the 2000-2016 time period. All factor models use EBIT/EV. QFM uses current EBIT while our proposed LFMs use predicted EBIT. Price-LSTM is trained to predict relative return.

Results

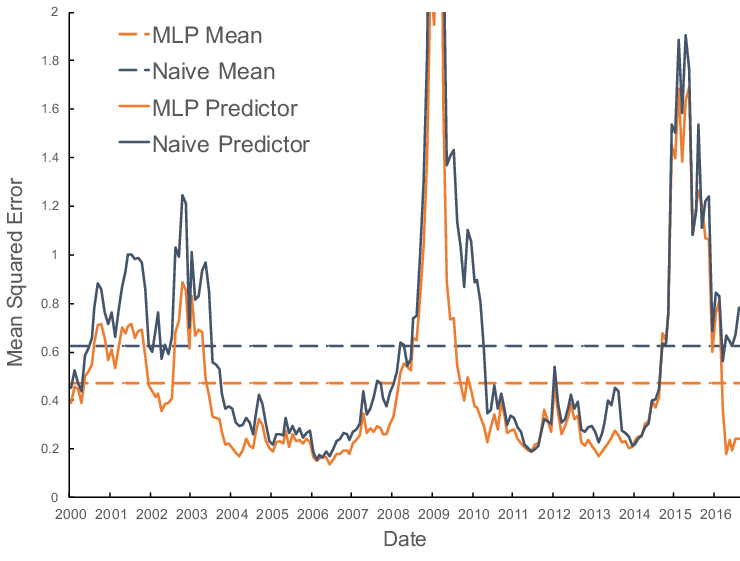

Quantitative analysis reveals that the proposed LFMs achieve a compounded annual return (CAR) of 17.1%, compared to only 14.4% for conventional factor models, and yield a Sharpe ratio of 0.68 versus 0.55. The superior performance of LFM leveraged by neural networks is further corroborated by reduced mean squared errors (MSE) in out-of-sample forecasts, demonstrating robustness across varied market conditions.

Implications and Future Work

This research suggests that forecasting future financial data provides a robust alternative to traditional quantitative investing models. The clear improvement in portfolio performance indicates that focusing on fundamental data and its projections can capture intrinsic value more accurately than using present data alone. This approach implies a fundamental shift towards employing prediction models in market forecasting, driving future advancements in algorithmic trading.

Future research directions include a comparative analysis between LFMs and direct price prediction models, examinations of different temporal windows and their influence on model predictions, and an evaluation of other fundamental data and its impacts on investment strategies.

Conclusion

The paper presents a novel application of deep learning models in financial prediction, successfully bypassing the limitations of conventional factor models by providing foresight into fundamental data. Through comprehensive simulation, the LFMs not only demonstrate impressive returns but also offer a pioneering approach for integrating AI in financial investments, encouraging further exploration and potential shifts in quantitative finance paradigms.