- The paper presents an innovative method that replaces differentiating the conditional expectation with applying the adjoint differential to streamline computations.

- It demonstrates effective calculation of Bermudan digital option deltas, reducing biases seen in traditional finite difference approximations.

- The study leverages minimal code modifications via the finmath-lib framework, offering flexibility in conditional expectation estimation for complex derivatives.

Automatic Backward Differentiation for American Monte-Carlo Algorithms (Conditional Expectation)

Introduction

The paper "Automatic Backward Differentiation for American Monte-Carlo Algorithms (Conditional Expectation)" presents an innovative approach to handling automatic differentiation in algorithms that involve conditional expectation operations. The research primarily addresses the computational challenges associated with estimating conditional expectations in Monte-Carlo simulations, widely used in financial mathematics for valuing complex derivatives such as Bermudan options.

Methodology

This study introduces a sophisticated method that allows for automatic backward differentiation in algorithms with conditional expectation operators. The key insight is to replace the differentiation of the conditional expectation operator with the application of the conditional expectation to the adjoint differential. This technique leverages three fundamental properties:

- Differentiation involving conditional expectations results in a linear combination of these operators.

- The differential of an expectation function translates into the expectation of the differential.

- The conditional expectation can be applied directly to the adjoint differential when focusing on the expectation of the final derivative result.

By using this methodology, the implementation complexity is significantly reduced while maintaining general applicability across various types of financial products.

Numerical Results

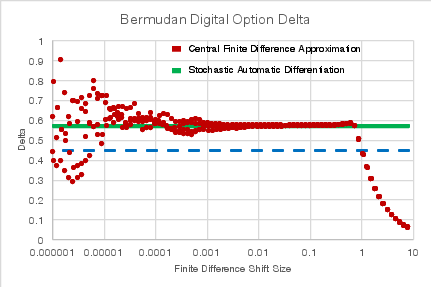

The effectiveness of the proposed method is demonstrated through the calculation of the delta of a Bermudan digital option. The chosen test case is an accurate reflection of the methodology’s capability to handle conditional expectations, which only appear within indicator functions.

Figure 1: Delta of a Bermudan digital option using finite differences (red) and stochastic AAD. The calculations were repeated with 4 different Monte-Carlo random number seeds.

The resolution of biases that arise in traditional finite difference approximation is evident in the depicted results. This highlights the article's premise that differentiating the approximation directly may not provide an accurate representation of the differential.

Implementation Strategy

The implementation of the outlined methodology is facilitated by the "finmath-lib" framework. The technique requires minimal additional code—specifically, enabling the tracking of conditional expectations in the operator tree through the getConditionalExpectation method. This aspect underscores the practical viability of deploying the approach without extensive code modifications.

The library extension leverages standard programming practices such as interfaces to integrate with existing Monte-Carlo simulation architectures seamlessly. The primary adjustment involves differentiating the conditional expectation estimator from its approximation, enhancing computational precision and efficiency.

Conclusion

The paper provides a comprehensive examination of implementing backward automatic differentiation in the context of American Monte-Carlo algorithms. Several advantages are identified:

- Avoidance of approximating differentials directly: This circumvents potential inaccuracies associated with differentiating approximations, such as piece-wise constant bins.

- Flexibility in choosing different conditional expectation estimation techniques for valuation and differentiation, potentially leading to improved result accuracy.

The research asserts crucial implications for simplifying computational implementations in financial valuations, especially in complex scenarios involving conditional expectations. Future work might explore extending these concepts to broader applications beyond financial derivatives, enriching the computational strategy for handling dynamic simulation algorithms.